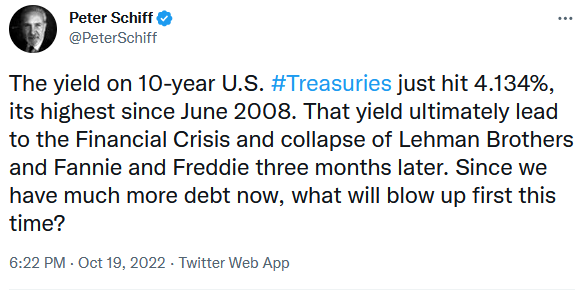

Ich glaub der Schiff erzählt mal wieder Scheiße.

Was hat 2008 mit Treasuries zu tun?

Was haben Hausbaukredite mit Treasuries zu tun??

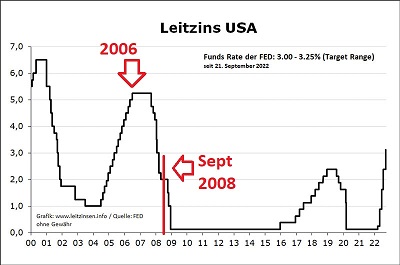

Hier ist die Kurve

https://en.wikipedia.org/wiki/…age_crisis_from_late_2007

The growth of private-label securitization and lack of regulation in this part of the market resulted in the oversupply of underpriced housing finance that led, in 2006, to an increasing number of borrowers, often with poor credit, who were unable to pay their mortgages -particularly with adjustable rate mortgages (ARM)- caused a precipitous increase in home foreclosures. As a result, home prices declined as increasing foreclosures added to the already large inventory of homes and stricter lending standards made it more and more difficult for borrowers to get mortgages.

[..], by August 2008, shares of both Fannie Mae and Freddie Mac had tumbled more than 90% from their one-year prior levels.

Was in dem tollen Wiki-Artikel gar nicht ewähnt wird:

am 29.06.2006 wurde der Leitzins auf 5,25 % erhöht.

"oversupply of underpriced housing finance" und "stricter lending standards" war lediglich Vorbereitung.

https://en.wikipedia.org/wiki/…anuary_2007_to_March_2008

As U.S. housing prices began to fall from their 2006 peak, global investors became less willing to invest in mortgage-backed securities (MBS). The crisis began to affect the financial sector in February 2007, when HSBC, one of the world's largest banks, said its charge for bad debts would be $10.5 billion, 20% higher than expectations. The increase was driven by increased expected losses in its US mortgage portfolio; this was the first major subprime related loss to be reported. By April 2007, over 50 mortgage companies had declared bankruptcy, many of which had specialized in subprime mortgages, [..]

The major investment banks had also increased their own borrowing and investing as the bubble expanded, taking on additional risk in the search for profit. For example, as of November 30, 2006, Bear Stearns reported $383.6 billion in liabilities and $11.8 billion in equity, a leverage ratio of approximately 33. This high leverage ratio meant that only a 3% reduction in the value of its assets would render it insolvent. Unable to withstand the combination of high leverage, reduced access to capital, loss in the value of its MBS securities portfolio, and claims from its hedge funds, Bear Stearns collapsed during March 2008.

Es hat also 8 Monate gedauert, bis die ersten Nachrichten kamen. (Juni 06 bis Februar 07)

Und 20 Monate bis die erste Bank pleite war. (Juni 06 bis März 08)

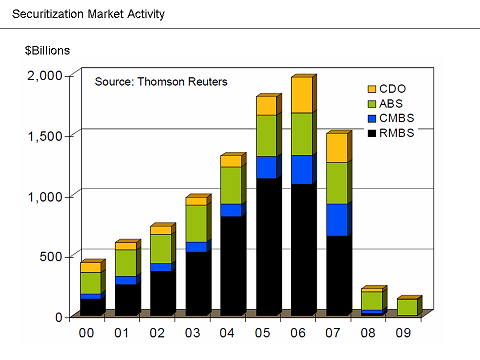

Wie man sieht, wurden noch in 2007 ne ganze Menge Kredite vergeben.

Bevor dann 2008 alles zu Ende ging

Bear Stearns wurde am 30.05.2008 von JPM übernommen, weil sonst Insolvenz.

Fannie Mae wurde im Juli 2008 staatlich gestützt, und zwar sehr kurzfrisitg.

Freddie Mac im Juli 2008 ebenso.

Lehmann Brs meldete am 15.09.2008 Insolvenz an.

Aktuell beträgt der Leitzins 3,25% und wird bestimmt weiter erhöht.

Es werden wohl kaum noch Kredite vergeben. (Bauland wird zurückgegeben, Angebot bei Immonet wird größer.) Wir dürften was die Kredite angeht bereits in "2007" angelangt sein

Interessant, daß der Ton jeweils im Februar und März gesetzt wurde, das passt zu meiner Übersicht hier.

Wenn Schiff doch irgendwie Recht hat, wären es 3 Monate wieder soweit: ~Februar 2023.

Die ersten Nachrichten (Credit Suisse, Deutsche, britische Rentenfonds) hatten wir schon? Aber nicht in Bezug auf den Hausmarkt, eher in Bezug auf Staatsanleihen.

Nochmal von oben

As a result, home prices declined as increasing foreclosures added to the already large inventory of homes and stricter lending standards made it more and more difficult for borrowers to get mortgages.

Im Januar 2023 kommt doch auch Basel III? Das sind doch auch striktere lending standards vorgesehen (nun bankenseitig). Und fallende Hauspreise wird es demnächst geben, daß ist für die Banken (equity) auch nicht gut.